IRS Form 656 is the foundation of any successful Offer in Compromise submission. If you are considering settling your federal tax debt for less than the full balance owed, understanding IRS Form 656 is not optional — it is essential. This is the official legal document that proposes your settlement to the Internal Revenue Service, outlines your offer amount, and establishes the basis for compromise under federal tax law. A single miscalculation, omission, or inconsistency on IRS Form 656 can result in an immediate return or rejection of your application.

As of 2026, the IRS has intensified financial verification procedures and documentation reviews. That means taxpayers who attempt to complete IRS Form 656 without fully understanding Reasonable Collection Potential (RCP), allowable expense standards, and compliance requirements face a significantly higher risk of denial. The form is rarely submitted alone; it must align precisely with detailed financial disclosures, supporting documentation, and strict procedural rules.

At Tax Law Advocates, our attorneys, CPAs, and IRS Enrolled Agents have extensive experience representing individuals and business owners before Revenue Officers and Offer in Compromise specialists. We do not simply “fill out paperwork.” We analyze asset equity, project future income using IRS methodology, anticipate potential expense disallowances, and structure offers designed to withstand scrutiny. In our experience, many rejected cases involve improperly calculated offers or incomplete disclosures on IRS Form 656.

If you are facing collection notices, wage garnishment threats, or escalating penalties, preparing IRS Form 656 strategically , not reactively , can make the difference between acceptance and prolonged enforcement. Understanding the legal, financial, and procedural framework behind IRS Form 656 is the first step toward resolving your tax liability responsibly and effectively.

What Is an IRS Offer in Compromise?

An Offer in Compromise (OIC) is a formal agreement between a taxpayer and the Internal Revenue Service that allows eligible individuals or businesses to settle tax debt for less than the full amount owed. The legal vehicle used to request this relief is IRS Form 656, which serves as the official written proposal submitted to the government. Without properly completing and filing IRS Form 656, the IRS will not evaluate your settlement request.

The IRS does not accept reduced settlements simply because a taxpayer asks. Approval depends on whether the offer equals or exceeds the taxpayer’s Reasonable Collection Potential (RCP) , a calculation based on asset equity and projected future income. When submitting IRS Form 656, the offer amount must be carefully calculated using IRS methodology. If the amount proposed is lower than what the IRS believes it can collect through enforced measures such as levies or installment agreements, the offer will likely be rejected.

The authority for this program comes from Internal Revenue Code §7122, which grants the IRS discretion to compromise tax liabilities under defined circumstances. However, the burden of proof is on the taxpayer. IRS Form 656 requires detailed financial disclosure and must align precisely with supporting documentation, including collection information statements and verification of income, expenses, and assets.

There are three legally recognized grounds for submitting IRS Form 656:

1. Doubt as to Collectibility

This is the most common basis for filing IRS Form 656. Under this ground, the IRS agrees that the tax debt is legally owed but determines that it is unlikely to collect the full amount within a reasonable period of time. If your net asset equity and disposable income are insufficient to satisfy the debt in full, an Offer in Compromise may be considered.

2. Doubt as to Liability

In this situation, IRS Form 656 is used when there is a legitimate dispute regarding whether the tax is actually owed. This may arise from audit errors, incorrect assessments, or misapplied payments. Unlike collectibility cases, this ground focuses on the legal validity of the liability itself rather than financial hardship.

3. Effective Tax Administration

Even if a taxpayer technically has the ability to pay, exceptional circumstances may justify compromise. Serious medical conditions, disability, or advanced age can support submission of IRS Form 656 under Effective Tax Administration if full payment would create significant economic hardship or would be inequitable under the circumstances.

Understanding these legal grounds is critical before preparing IRS Form 656. Filing without meeting one of these standards increases the risk of rejection and wasted time. A strategic evaluation of eligibility ensures the Offer in Compromise process begins on solid legal footing.

What’s Changed Recently (2026 Update)

As of 2026, taxpayers preparing an Offer in Compromise must be even more precise when completing IRS Form 656 and related financial disclosures. Several procedural and economic updates now directly impact how the Internal Revenue Service evaluates settlements and calculates Reasonable Collection Potential (RCP).

First, the IRS has implemented inflation-adjusted National and Local Standards for allowable living expenses. These standards determine how much of your income is considered necessary for housing, food, transportation, and utilities when calculating disposable income. Because IRS Form 656 must align with Collection Information Statements (Form 433-A(OIC) or 433-B(OIC)), even small discrepancies between reported expenses and updated IRS standards can result in proposed rejections or reduced allowable amounts.

Second, the IRS has strengthened its financial verification protocols. Offer specialists are now cross-checking bank deposits, credit card activity, digital payment platforms, and third-party reporting forms such as 1099-K more aggressively. When submitting IRS Form 656, taxpayers must ensure that all income sources , including gig work, online sales, and side businesses — are fully disclosed. Inconsistent reporting is a leading cause of returned or rejected applications.

Third, there is expanded scrutiny of digital assets. Cryptocurrency holdings, online brokerage accounts, and alternative investments must be reported as part of asset disclosures tied to IRS Form 656. Failure to disclose digital holdings can result in immediate denial and potential penalties.

Finally, continued IRS enforcement funding has increased staffing in collection divisions. Revenue Officers are reviewing Offer in Compromise submissions with heightened attention to documentation completeness. Recent IRS procedural updates emphasize that incomplete or inconsistent financial forms accompanying IRS Form 656 are more likely to be returned without evaluation.

In 2026, accuracy, transparency, and full documentation are no longer optional , they are essential to a defensible Offer in Compromise strategy.

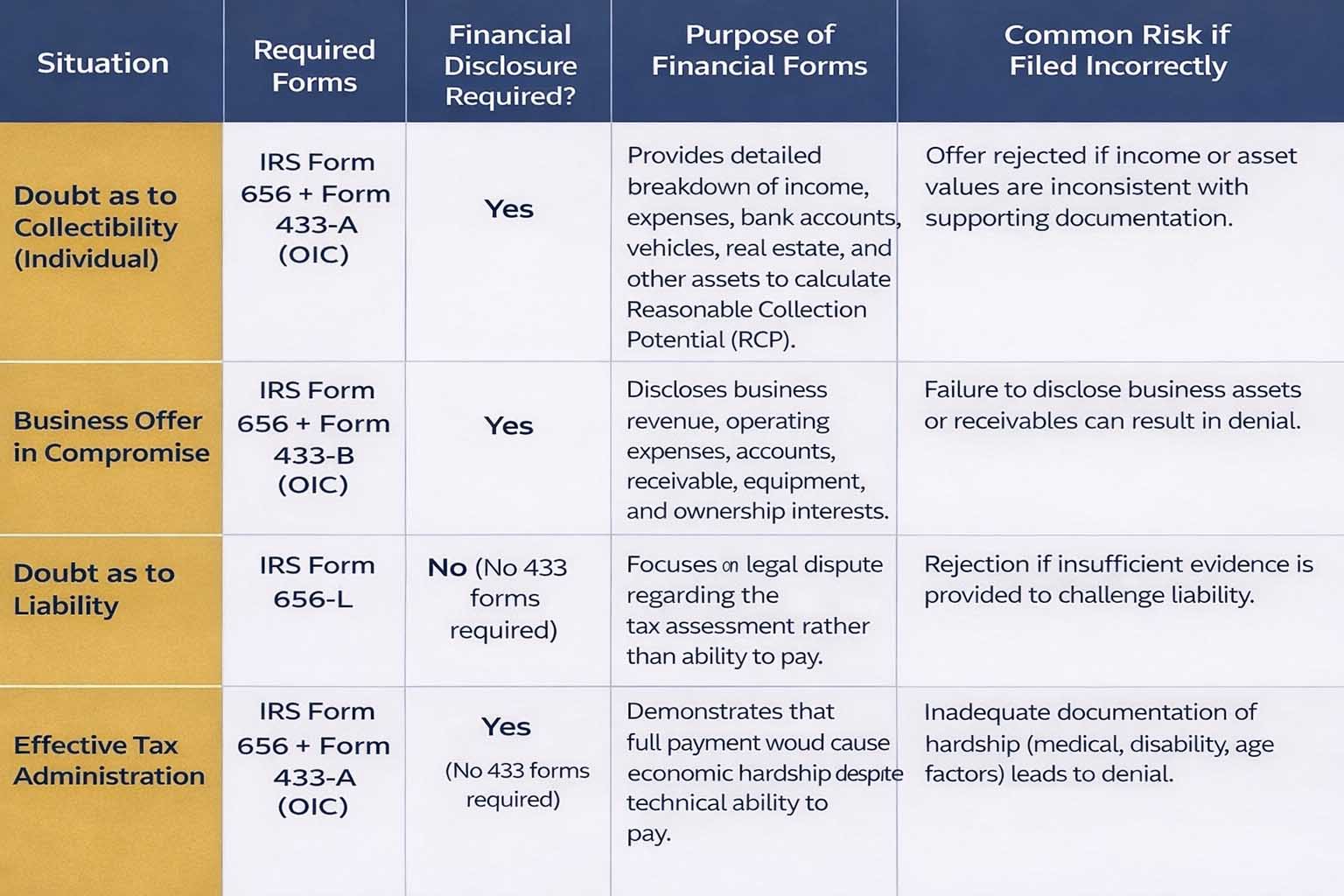

Required Forms Overview (2026)

Before submitting an Offer in Compromise in 2026, understanding which documents are required is critical. The IRS will not evaluate a settlement request unless the correct version of IRS Form 656 is filed with the appropriate financial disclosures. Each legal basis for compromise requires a different combination of forms, and submitting the wrong package is one of the most common reasons applications are returned without review. In addition to IRS Form 656, most applicants must provide detailed financial statements that disclose income, assets, liabilities, and monthly expenses. The table below outlines the required forms depending on your specific situation.

How the IRS Calculates Your Offer (RCP Formula)

When evaluating an Offer in Compromise, the IRS does not negotiate emotionally , it calculates mathematically. The foundation of every decision is the taxpayer’s Reasonable Collection Potential (RCP). If your offer does not meet or exceed this number, it will likely be rejected.

The RCP formula is straightforward in structure but complex in application:

RCP = Net Realizable Equity in Assets + Future Income Potential

1. Net Realizable Equity in Assets

The IRS determines what your assets could realistically sell for in a quick-sale scenario (typically around 80% of fair market value), then subtracts any secured debt. This includes:

- Real estate

- Vehicles

- Bank accounts

- Investment accounts

- Business assets

- Cryptocurrency holdings

Lead attorneys at Tax Law Advocates advise clients that one of the most common mistakes is undervaluing assets or failing to account for equity correctly. IRS examiners independently verify property values, loan balances, and financial account activity. Inconsistent valuations can undermine credibility immediately.

2. Future Income Potential

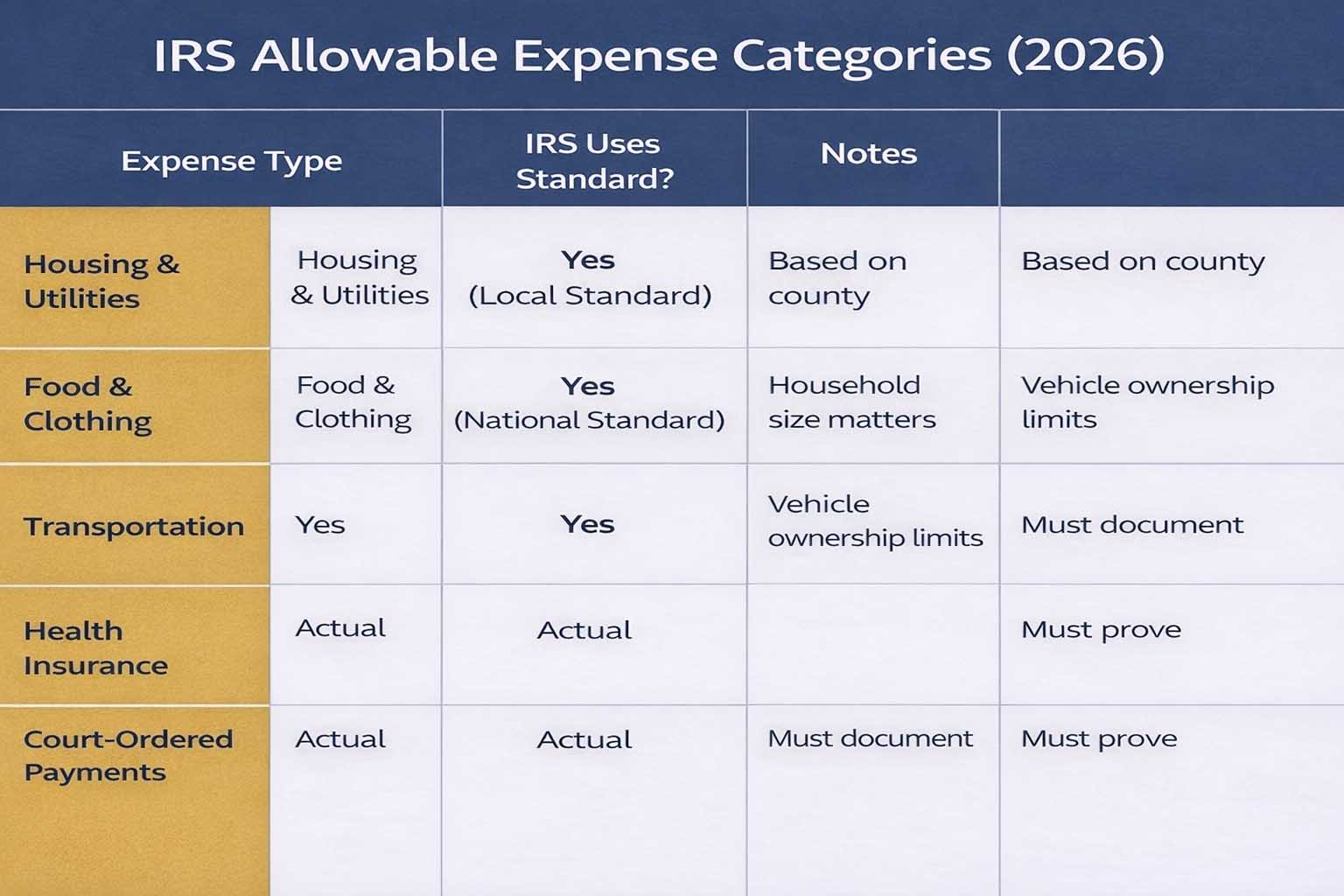

The second component is your projected disposable income. The IRS calculates this by subtracting allowable living expenses (based on National and Local Standards) from your gross monthly income. The remaining amount is multiplied by 12 or 24 months, depending on the payment option selected.

Our lead attorneys emphasize that “allowable expenses” are not simply what you actually spend. The IRS applies standardized limits, and expenses exceeding those guidelines are often reduced. Strategic preparation requires understanding how to properly document necessary deviations, such as medical conditions or special family circumstances.

In our experience representing taxpayers before Revenue Officers and OIC specialists, the key to a successful Offer in Compromise is not just computing the RCP , it’s presenting defensible documentation that supports each component of the calculation. Precision, consistency, and proactive explanation make the difference between acceptance and rejection.

IRS Allowable Expense Categories (2026)

Step-by-Step: Submitting Form 656 in 2026

(Strategic Guidance from Tax Law Advocates)

Filing Form 656 in 2026 requires far more than filling in blanks and mailing paperwork. The IRS has strengthened financial verification procedures, increased enforcement staffing, and tightened documentation review standards. In our experience at Tax Law Advocates, successful Offer in Compromise submissions are built on preparation, calculation accuracy, and strategic presentation , not guesswork.

Below is the professional framework we use when guiding clients through the process.

1. Calculate a Defensible Offer

Before completing Form 656, you must determine your Reasonable Collection Potential (RCP). This calculation includes asset equity and projected future disposable income.

Our attorneys emphasize that offering “what feels affordable” is not sufficient. The IRS uses a formula. If your offer is below the calculated RCP, it will almost certainly be rejected.

We routinely review:

- Quick-sale value of assets

- Loan balances

- Allowable expense standards

- Income consistency across tax returns and bank statements

Precision at this stage prevents costly rejection later.

2. Choose the Correct Payment Type

Form 656 requires selecting a payment option:

Lump Sum Cash Offer

- 20% of the total offer must be submitted with the application

- Remaining balance paid in five or fewer payments within 24 months

Periodic Payment Offer

- Initial payment submitted with application

- Monthly payments continue while IRS reviews the offer

From a strategy perspective, our firm evaluates cash flow, risk tolerance, and enforcement posture before advising which option is appropriate. In some cases, periodic payments can create financial strain if review time extends beyond expectations.

3. Complete All Forms Accurately

Every field must be addressed. Write “N/A” where appropriate — never leave blanks.

We often see returns triggered by:

- Inconsistent income reporting

- Missing asset disclosures

- Mathematical errors

- Discrepancies between Form 656 and Form 433-A (OIC)

In 2026, cross-verification with third-party data has increased. Transparency is essential.

4. Attach Supporting Documentation

Supporting documents validate your disclosures. These may include:

- Pay stubs

- Bank statements

- Mortgage balances

- Vehicle loan documents

- Medical expense records

IRS examiners expect documentation that matches your reported figures exactly.

5. Include the $205 Application Fee (Unless Exempt)

Most applicants must include the non-refundable $205 fee. Low-income certification may qualify you for exemption, but eligibility must be carefully verified.

6. Mail to the Correct IRS Processing Center

Submission addresses vary by state and type of offer. Always confirm the current IRS instructions before mailing.

Critical Warning

Incomplete submissions are returned , not formally rejected , and the application fee is forfeited. This causes delays, additional penalties accrual, and potential enforcement escalation.

In our experience representing taxpayers before Revenue Officers and OIC specialists, careful preparation is the difference between strategic review and procedural setback.

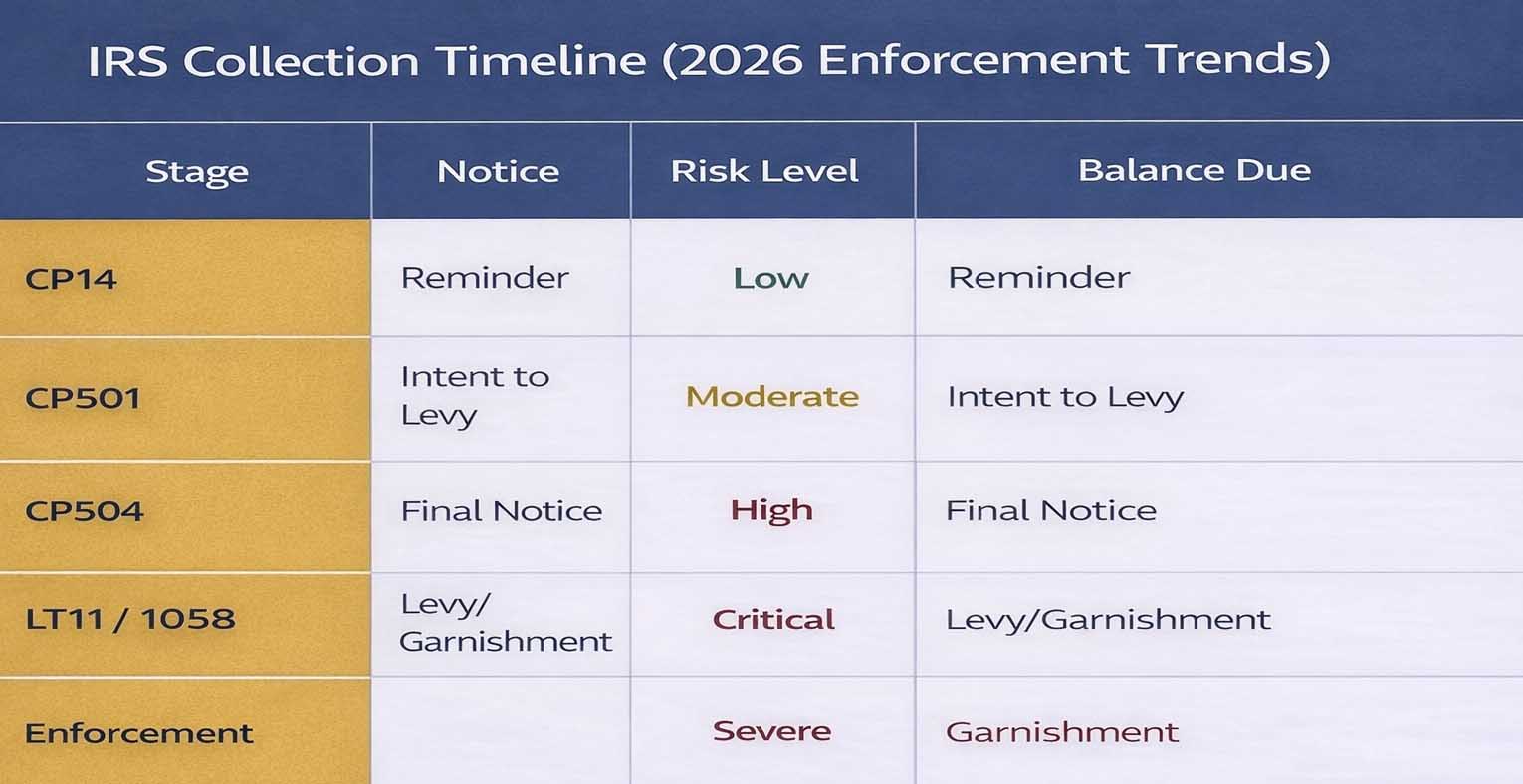

IRS Collection Timeline (2026 Enforcement Trends)

What Happens After Filing?

1. Pending Status

Collection activity generally pauses.

2. Financial Investigation

IRS specialist verifies income, expenses, assets.

3. Proposed Rejection (if applicable)

You may respond or increase the offer.

4. Appeal Rights

30 days to appeal to the IRS Independent Office of Appeals.

Common Taxpayer Mistakes (Risk Analysis)

- Underreporting bank deposits

- Offering less than calculated RCP

- Inflating expenses beyond IRS standards

- Missing documentation

- Filing while non-compliant with current tax returns

In our experience representing taxpayers before Revenue Officers, incomplete 433 forms are the #1 cause of failure.

DIY IRS Resolution vs Hiring a Tax Attorney (2026 Comparison)

Facing IRS collection action in 2026 can feel overwhelming. With online calculators, downloadable forms, and IRS publications readily available, many taxpayers ask: Can I handle this myself? The answer depends on the complexity of your case, your financial situation, and your tolerance for procedural risk. Below is a realistic comparison between pursuing IRS resolution on your own and hiring an experienced tax attorney.

Risk Level

Handling an Offer in Compromise, installment agreement, or penalty abatement request on your own carries procedural risk. The IRS applies strict financial standards and documentation rules. A small miscalculation in asset equity, allowable expenses, or income reporting can result in rejection , or worse, enforcement escalation.

When represented by a tax attorney, risk is reduced because submissions are prepared with strategic alignment to IRS guidelines. Attorneys anticipate objections, identify weak points, and ensure consistency across all financial disclosures.

Approval Probability

No professional can guarantee approval. However, historically, many rejected cases involve incomplete documentation, inaccurate financial statements, or offers calculated below Reasonable Collection Potential (RCP).

Tax attorneys understand how IRS settlement criteria are applied in practice. In our experience representing taxpayers before Revenue Officers and the Independent Office of Appeals, properly structured cases stand a stronger chance of surviving review.

Time Investment

DIY IRS resolution requires extensive time gathering documentation, studying IRS procedures, completing complex financial forms, and responding to follow-up requests. The review process can take months.

With representation, your attorney handles communication, document preparation, negotiation strategy, and response deadlines , allowing you to focus on work and family while maintaining compliance.

Documentation Complexity

IRS financial disclosures are detailed and technical. Expense categories must align with National and Local Standards. Asset valuations must be defensible.

An attorney ensures financial statements reflect IRS methodology , not simply household budgeting figures. This technical alignment is often where DIY filings fail.

Negotiation Leverage

When you represent yourself, you negotiate directly with the IRS examiner assigned to your case. While IRS employees are professional, they apply internal guidelines rigorously.

A tax attorney brings experience negotiating with the IRS, understanding internal procedures, escalation pathways, and appeal rights. Representation signals that the case is being handled with legal oversight.

Long-Term Compliance Protection

An accepted Offer in Compromise requires five years of strict compliance. Missed filings or late payments can default the agreement and reinstate the full original debt.

Professional guidance helps structure not only resolution , but future compliance planning to prevent recurrence.

Why Experience Matters in IRS Cases

IRS OIC specialists are trained financial analysts. They look for inconsistencies.

In our representation work:

- We anticipate expense disallowances

- We structure future income projections properly

- We prepare rebuttals to proposed rejections

- We protect against enforcement escalation

The difference is preparation and procedural fluency.

Realistic Acceptance Rates

Historically, the IRS accepts fewer than half of submitted offers.

Common rejection reasons:

- Ability to pay via installment agreement

- Offer below RCP

- Missing compliance

- Incomplete documentation

Take Action Before the IRS Escalates

If you have received CP504 or LT11 notices, levy action may follow.

Delays increase penalties and interest daily.

Free consultations are available to evaluate:

- OIC eligibility

- Alternative resolutions

- Enforcement risk level

Frequently Asked Questions

Q1: How long does an Offer in Compromise take in 2026?

In 2026, most Offer in Compromise cases take 6 to 12 months, though complex cases can take longer. Processing time depends on IRS workload, completeness of documentation, and whether additional financial verification is required. At Tax Law Advocates, we help ensure submissions are complete and strategically prepared to reduce unnecessary delays and avoid procedural returns.

Q2: Does filing an Offer in Compromise stop wage garnishment?

Generally, yes. Once the IRS accepts your Offer in Compromise as “pending,” most collection actions , including wage garnishments and bank levies , are typically suspended. However, timing matters. If enforcement is already active, immediate professional intervention may be necessary. Tax Law Advocates routinely communicate directly with IRS collection units to confirm enforcement holds are properly applied.

Q3: Can I submit an Offer in Compromise without paying the application fee?

Most applicants must submit the $205 application fee and an initial payment. However, low-income taxpayers may qualify for a fee waiver based on IRS income thresholds. Determining eligibility requires careful review of household income and family size. Our team evaluates exemption eligibility before submission to prevent returned applications.

Q4: What happens if my Offer in Compromise is rejected?

If the IRS rejects your offer, you generally have 30 days to file an appeal with the IRS Independent Office of Appeals. This stage is critical. Appeals require structured argument, financial clarification, and sometimes recalculated Reasonable Collection Potential. Tax Law Advocates provides representation during appeals to strengthen negotiation positioning.

Q5: Do penalties and interest stop during the review process?

No. Interest and penalties generally continue accruing until the settlement is finalized or the debt is fully resolved. Understanding how accrual impacts overall liability is part of strategic case planning at Tax Law Advocates.

Conclusion: Resolve Your Tax Debt with Confidence

IRS debt does not resolve itself , and ignoring collection notices only increases penalties, interest, and enforcement risk. In 2026, with stronger verification protocols, expanded enforcement staffing, and heightened scrutiny of financial disclosures, navigating an Offer in Compromise or other IRS resolution strategy requires precision and strategic planning.

Whether you are considering submitting IRS Form 656, negotiating an installment agreement, requesting penalty relief, or responding to a Final Notice of Intent to Levy, timing and preparation matter. A single procedural mistake can result in rejection, returned applications, or accelerated enforcement such as wage garnishment or bank levies.

At Tax Law Advocates, our attorneys, CPAs, and IRS Enrolled Agents have extensive experience representing taxpayers before Revenue Officers, Automated Collection units, and the IRS Independent Office of Appeals. We understand how Reasonable Collection Potential is calculated, how allowable expense standards are applied, and how to prepare documentation that withstands scrutiny. Our approach is strategic, compliant, and grounded in real-world IRS representation experience.

No firm can guarantee results , and you should be cautious of anyone who does. But informed, professional representation significantly reduces risk and increases procedural strength.

If you are facing IRS collection action or considering an Offer in Compromise, now is the time to act , before enforcement escalates.

Schedule your confidential consultation with Tax Law Advocates today.

OFFICE HOURS: Monday-Thursday 7:00 A.M. to 5:00 P.M. PST Friday 7:00 A.M. to 4:00 P.M. PST

Talk to a qualified tax expert now: 855-612-7777

Let our experienced team evaluate your situation, explain your options clearly, and help you move toward resolution with stability and confidence.

Important Legal Disclaimer (Updated 2026)

This article is informational only and not legal advice. Acceptance of an Offer in Compromise depends on documented financial circumstances and IRS evaluation. No outcome can be guaranteed. Always consult a licensed tax attorney, CPA, or enrolled agent before submitting Form 656. Tax Law Advocates is not affiliated with the IRS.

About the Author: David Cho

As the Lead Tax Attorney at Tax Law Advocates, David Cho provides expert guidance on federal and state tax resolution matters. He earned both his J.D. and LL.M. in Taxation from the University of California, Irvine School of Law, building a strong foundation for his practice. David is passionate about delivering practical solutions that directly and positively impact his clients’ livelihoods, and he excels at working collaboratively with the IRS and state agencies to achieve favorable outcomes. His dedication is evident in his work, such as when he assisted a client who had fallen victim to a tax scam. By preparing and submitting a strategic Offer in Compromise, David helped her pursue resolution and take meaningful steps toward financial recovery. His deep knowledge of the IRS Debt Forgiveness Program makes him a vital resource for taxpayers facing significant challenges.