Currently Not Collectible (CNC) status can be a lifeline when IRS notices begin arriving and you’re already struggling to cover rent, groceries, utilities, and other basic living expenses. For many taxpayers, the fear escalates quickly , wage garnishment, bank levies, federal tax liens, and mounting penalties create overwhelming pressure. But when financial hardship is real and documented, Currently Not Collectible (CNC) status may temporarily pause IRS collection activity and provide critical breathing room.

At Tax Law Advocates, we have represented financially distressed taxpayers before Revenue Officers, the Automated Collection System (ACS), and the IRS Office of Appeals. In our experience, securing Currently Not Collectible (CNC) status requires more than simply telling the IRS you cannot pay. It demands detailed financial analysis under IRS Collection Financial Standards, proper documentation of income and allowable expenses, and strategic positioning of the case before enforcement escalates. When handled correctly, Currently Not Collectible (CNC) status can stop levies and garnishments , but when handled improperly, it can lead to denial or continued enforcement.

As of 2026, Currently Not Collectible (CNC) status remains one of the most misunderstood , and most powerful , IRS hardship protections available to taxpayers facing genuine economic hardship. IRS enforcement has become more automated, and financial disclosures are reviewed closely. The IRS evaluates disposable income, equity in assets, allowable expense categories, and overall collection potential before granting hardship status. Simply being unable to pay in full does not automatically qualify a taxpayer.

In our practice, we often see individuals attempt to apply for Currently Not Collectible (CNC) status without reviewing their transcripts, calculating allowable living expenses under IRS guidelines, or understanding how asset equity impacts eligibility. This can delay relief or create unnecessary complications. A properly structured submission anticipates IRS scrutiny and addresses financial documentation before questions arise.

IRS hardship Updated for 2026: What’s Changed Recently?

As of 2026, IRS hardship enforcement and financial review procedures have evolved in ways that directly impact taxpayers seeking Currently Not Collectible (CNC) status. While the core legal framework remains intact, collection strategy, automation systems, and financial scrutiny standards have become more structured and data-driven. Understanding these updates is critical before requesting Currently Not Collectible (CNC) status.

Below are the key changes and enforcement trends affecting hardship cases in 2026.

Increased IRS Automation and Faster Collection Escalation

One of the most significant changes is the continued expansion of automated collection systems. IRS notices such as CP14, CP501, CP503, and CP504 are now issued more quickly after assessment. The timeline between an initial balance due notice and a Final Notice of Intent to Levy has shortened in many cases.

For taxpayers who may qualify for Currently Not Collectible (CNC) status, this means waiting too long can result in wage garnishment or bank levies before hardship relief is formally requested. Acting early is more important than ever.

Stricter Financial Disclosure Review (Form 433 Standards)

The IRS continues applying detailed financial analysis when reviewing hardship requests. In 2026, Revenue Officers and Automated Collection System representatives are carefully evaluating:

- Monthly income verification

- Allowable living expenses under IRS Collection Financial Standards

- Bank statements and asset equity

- Cryptocurrency and digital asset disclosures

Simply stating financial difficulty is insufficient. To obtain Currently Not Collectible (CNC) status, taxpayers must demonstrate that paying the IRS would prevent them from meeting necessary living expenses as defined by IRS guidelines.

Inflation Adjustments to Allowable Expense Standards

IRS National and Local Standards for housing, transportation, and living expenses are adjusted periodically for inflation. In 2026, these updated thresholds may slightly increase allowable expense caps in certain regions.

This can affect eligibility calculations for Currently Not Collectible (CNC) status because allowable expenses determine whether a taxpayer has disposable income available for payment. Accurate calculation using current standards is essential.

Expanded Digital Monitoring and Income Matching

The IRS has enhanced third-party reporting integration, including 1099-K reporting, gig economy platforms, and digital asset transactions. Financial discrepancies may trigger faster compliance review.

Taxpayers requesting Currently Not Collectible (CNC) status should ensure that all filed returns are accurate and current. Open or unfiled returns often delay hardship consideration.

Continued Focus on Payroll and Trust Fund Enforcement

While hardship protections remain available, the IRS continues prioritizing employment tax enforcement. Business owners seeking Currently Not Collectible (CNC) status for payroll liabilities may face deeper financial review and potential Trust Fund Recovery Penalty investigations.

Documentation and strategic preparation are critical in these cases.

Ongoing Review of CNC Accounts

Many taxpayers assume that once hardship status is granted, the matter is permanently resolved. However, in 2026 the IRS continues periodic financial reviews of accounts placed in Currently Not Collectible (CNC) status. If income increases or assets are acquired, collection activity may resume.

The 2026 enforcement environment emphasizes documentation, timeliness, and procedural precision. While Currently Not Collectible (CNC) status remains a powerful protection for taxpayers experiencing genuine hardship, the standards for approval are carefully applied. Understanding these recent updates can significantly improve your chances of obtaining and maintaining relief.

What Does Currently Not Collectible (CNC) Status Mean?

When taxpayers hear the term hardship or uncollectible account, confusion is common. Currently Not Collectible (CNC) status is a formal IRS classification that temporarily pauses active collection when a taxpayer demonstrates that paying their tax debt would prevent them from covering necessary living expenses. It does not erase the debt, but it can stop enforcement actions while financial hardship continues.

Understanding what Currently Not Collectible (CNC) status truly means , and what it does not mean , is critical before pursuing this relief option.

Temporary Suspension of IRS Collection Activity

The primary effect of Currently Not Collectible (CNC) status is that the IRS agrees to suspend active collection efforts. This typically means:

- Wage garnishments are halted

- Bank levies are released or not initiated

- Revenue Officer collection activity pauses

- Installment agreement payments are not required

However, penalties and interest generally continue accruing during hardship status. The underlying tax debt remains legally owed.

Financial Hardship Qualification Standards

The IRS does not grant Currently Not Collectible (CNC) status simply because a taxpayer cannot pay in full. The taxpayer must show that, after applying IRS Collection Financial Standards, there is no disposable income available to apply toward the tax debt.

The IRS reviews:

- Gross monthly income

- Necessary living expenses (housing, food, transportation, healthcare)

- Asset equity

- Bank balances

- Retirement accounts

- Business income (if applicable)

If allowable expenses equal or exceed income, hardship status may be approved.

Not a Forgiveness Program

A common misconception is that Currently Not Collectible (CNC) status eliminates the tax liability. It does not. The debt remains legally enforceable until:

- Paid in full

- Settled through Offer in Compromise

- Expired under the Collection Statute Expiration Date (CSED)

In some cases, taxpayers remain in hardship status until the statute expires. In other situations, the IRS re-evaluates financial conditions and resumes collection if circumstances improve.

Ongoing IRS Monitoring and Periodic Review

Accounts placed in Currently Not Collectible (CNC) status are subject to periodic review. The IRS may:

- Request updated financial information

- Monitor income reporting

- Review new W-2s or 1099s

- Identify asset acquisitions

If income increases or expenses decrease significantly, the IRS can remove hardship status and resume enforcement.

Impact on Federal Tax Liens and Credit

Although active levies may pause, a Notice of Federal Tax Lien may still be filed. Currently Not Collectible (CNC) status does not automatically remove an existing lien. This can affect credit reports and property transactions.

Strategic Use of Hardship Protection

For taxpayers facing genuine economic distress , unemployment, medical hardship, business collapse, or fixed income limitations . Currently Not Collectible (CNC) status can provide critical financial breathing room. It creates stability while long-term resolution options are evaluated.

Proper financial documentation, compliance with filing requirements, and accurate presentation of income and expenses are essential for approval. Understanding the scope and limits of hardship protection helps taxpayers make informed decisions about next steps and future tax planning.

When Currently Not Collectible Status May Help

You may qualify if:

- Your necessary expenses equal or exceed income

- You have no disposable income

- Your only income is Social Security, SSI, or limited benefits

- You are unemployed or medically unable to work

- You are facing eviction or utility shutoff

In our experience representing taxpayers before Revenue Officers, the strongest CNC cases involve:

- Clear documentation

- Proper classification of allowable expenses

- Accurate completion of Form 433-A or 433-F

- No missing tax returns

IRS Collection Timeline (Understanding the Risk)

When taxpayers fall behind on their federal tax obligations, the IRS follows a structured enforcement process. Understanding the IRS collection timeline is critical because each stage carries increasing financial and legal risk. In 2026, automated systems have shortened response windows, meaning delays can trigger faster escalation.

Below is a simplified breakdown of how collection typically progresses.

Stage 1: Initial Balance Due Notice (CP14)

The process usually begins with a CP14 Notice, which informs you of the tax owed, including penalties and interest.

At this stage:

- The IRS is requesting voluntary payment.

- No enforcement action has begun.

- Interest continues accruing daily.

This is the lowest-risk stage — and often the best time to explore resolution options such as installment agreements, penalty abatement, or hardship status.

Stage 2: Reminder Notices (CP501 / CP503)

If the balance remains unpaid, the IRS issues follow-up reminders.

Risk level increases because:

- The account is now flagged for potential enforcement.

- The IRS may begin reviewing financial records.

- Response urgency becomes more critical.

Ignoring these notices often leads to the next and far more serious phase.

Stage 3: Final Notice – CP504 (Intent to Levy)

The CP504 Notice signals that the IRS intends to levy certain assets if payment is not made.

At this point:

- The IRS may levy state tax refunds.

- Federal tax lien filing becomes more likely.

- The account is nearing active enforcement status.

While CP504 is serious, taxpayers still have time to act before broader levy authority begins.

Stage 4: Final Notice of Intent to Levy (Letter 1058 / LT11)

This is one of the most critical notices in the IRS collection timeline.

Key features:

- Grants a 30-day window to request a Collection Due Process (CDP) hearing.

- After 30 days, the IRS may legally garnish wages or levy bank accounts.

- Appeal rights expire if no action is taken within the deadline.

This stage represents a major turning point. Immediate action is often required to preserve legal rights.

Stage 5: Levy and Wage Garnishment

If no resolution is reached:

- Bank accounts may be frozen.

- Wages can be garnished.

- Social Security benefits may be levied (subject to limits).

Unlike private creditors, the IRS does not need a court judgment to levy once proper notice has been issued.

Federal Tax Lien Filing

Separately from levies, the IRS may file a Notice of Federal Tax Lien.

Consequences include:

- Damage to credit profile

- Public record of tax debt

- Complications in selling or refinancing property

A lien secures the government’s claim against assets.

Collection Statute Expiration Date (CSED)

The IRS generally has 10 years from the date of assessment to collect a tax debt. However, certain actions — including bankruptcy, offers in compromise, and appeals — may suspend or extend this timeline.

Why Timing Matters in 2026

In 2026, timing is no longer just important in IRS cases , it is often the deciding factor between manageable resolution and aggressive enforcement. The Internal Revenue Service has continued expanding automation, digital income matching, and streamlined notice processing. This means accounts move through the collection system faster than in previous years, leaving taxpayers with narrower response windows.

Once a balance is assessed, penalties and interest begin accruing immediately. Failure-to-file and failure-to-pay penalties compound monthly, while statutory interest compounds daily. Even a short delay can significantly increase the total liability. Acting early can reduce exposure and, in some cases, limit how much additional penalty accrues.

More critically, enforcement notices now progress more efficiently through automated systems. When a Final Notice of Intent to Levy is issued, taxpayers typically have 30 days to request a Collection Due Process (CDP) hearing. Missing that deadline may eliminate appeal rights and allow the IRS to garnish wages or levy bank accounts without further court involvement. In 2026, missed deadlines often result in faster levy action.

Timing also affects eligibility for relief options. Certain programs , such as installment agreements, penalty abatement, or hardship status , are easier to secure before enforcement escalates. Once a Revenue Officer is assigned, documentation standards may become stricter and negotiations more formal.

Additionally, delays can complicate long-term planning. The IRS generally has a 10-year collection statute, but certain actions can suspend or extend that period. Strategic timing helps protect that statute and avoid unnecessary extensions.

In today’s enforcement environment, early intervention provides leverage, preserves appeal rights, and expands resolution options. Waiting reduces flexibility. Acting promptly protects both finances and legal position.

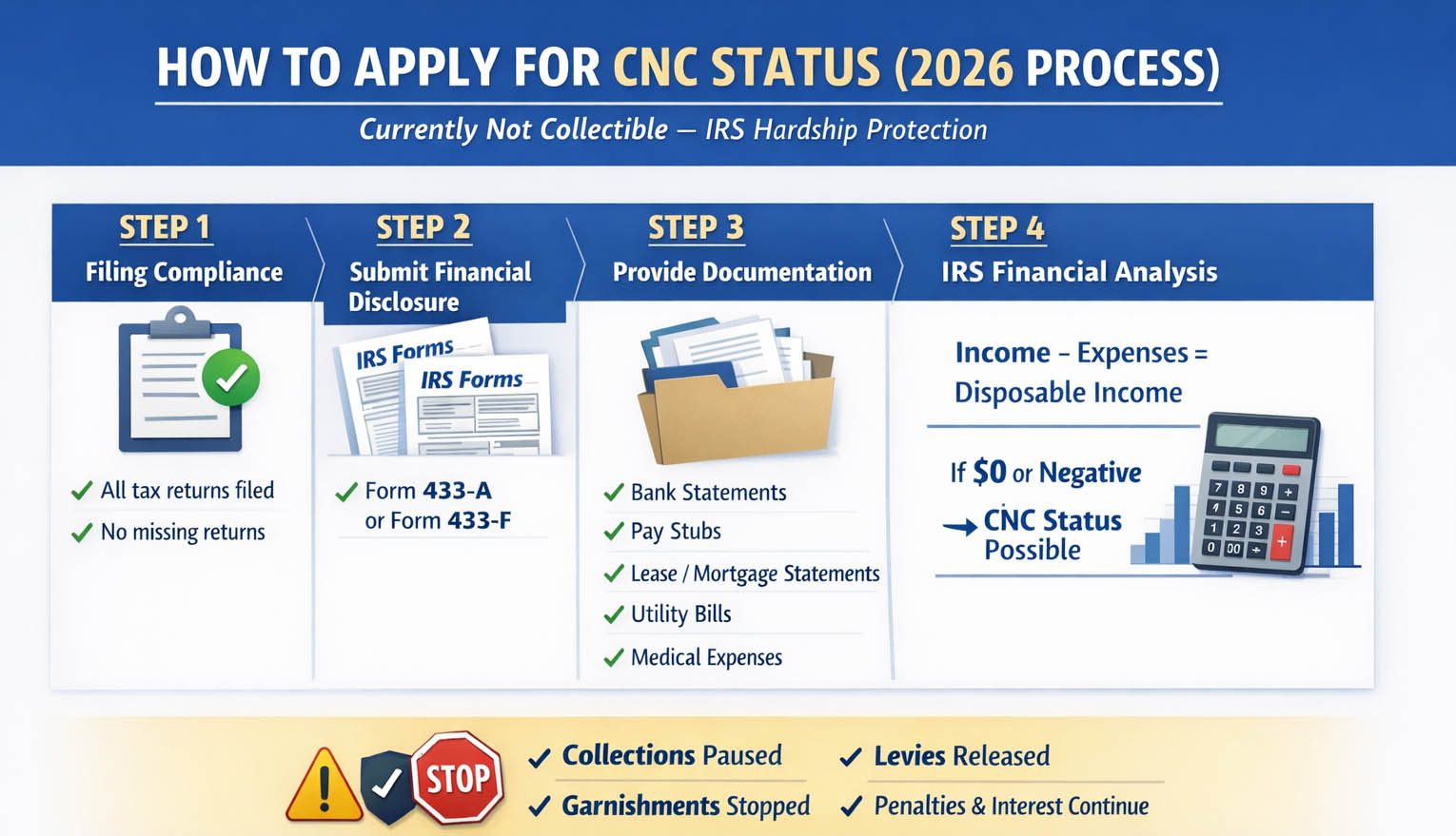

Step-by-Step: How to Apply for CNC Status (2026 Process)

Step 1: Ensure Filing Compliance

All required tax returns must be filed.

Step 2: Complete a Collection Information Statement

- Form 433-A (Wage Earners / Self-Employed)

- Form 433-F (Streamlined financial review)

Step 3: Provide Documentation

- Bank statements

- Pay stubs

- Lease/mortgage statements

- Utility bills

- Medical expense proof

Step 4: IRS Financial Analysis

The IRS compares:

Income – Allowable Expenses = Disposable Income

If disposable income = $0 or negative → CNC may be granted.

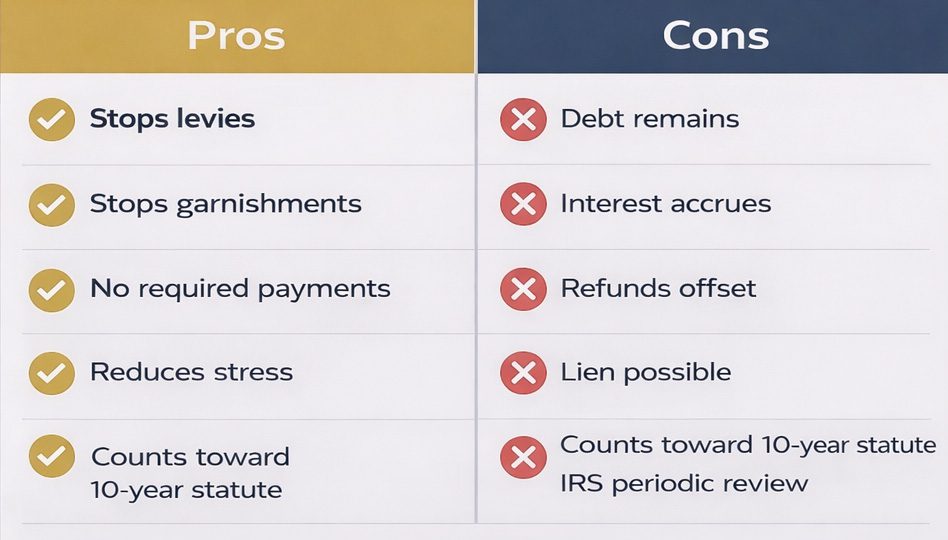

Pros and Cons of CNC Status

How Long Does CNC Status Last?

CNC ends when:

- Financial condition improves

- IRS reviews and removes hardship

- The Collection Statute Expiration Date (CSED) expires (generally 10 years from assessment)

Time in CNC typically counts toward the CSED.

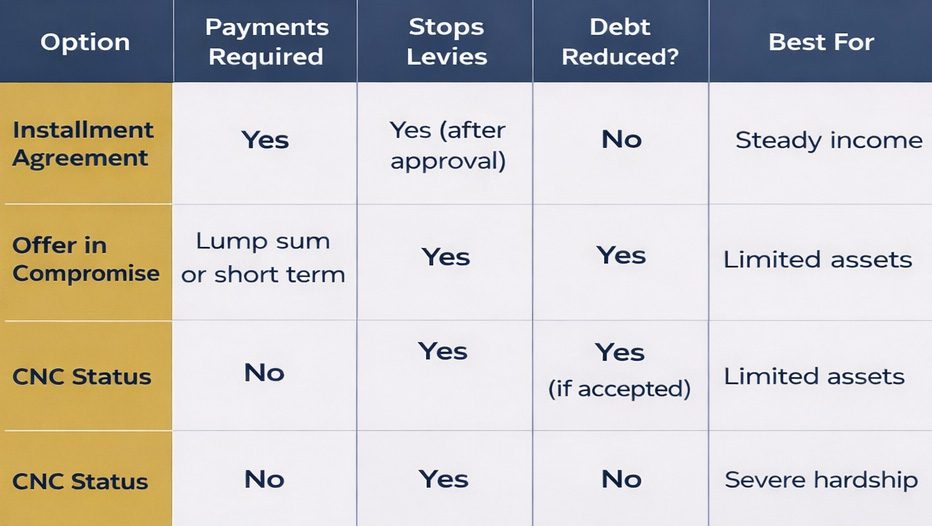

IRS Resolution Options Comparison (2026)

DIY IRS Resolution vs Hiring a Tax Attorney (2026 Comparison)

When facing IRS debt in 2026, many taxpayers ask the same question: Should I handle this myself, or should I hire a tax attorney? The answer depends on complexity, risk level, and how much financial exposure is involved. With faster enforcement timelines and expanded automation, the difference between DIY resolution and professional representation has become more significant.

Below is a strategic comparison to help you evaluate both paths.

Risk Level and Exposure

Handling an IRS matter yourself may be reasonable for small balances with no enforcement notices. For example, setting up a basic online installment agreement for a modest debt can sometimes be done without professional assistance.

However, once penalties accumulate, liens are filed, or levy notices are issued, the risk increases. A tax attorney understands procedural deadlines, appeal rights, and collection statutes. In 2026, missing a 30-day window after a Final Notice of Intent to Levy can eliminate certain appeal protections. That level of risk often warrants experienced guidance.

Documentation and Financial Disclosure Complexity

DIY taxpayers often underestimate how detailed IRS financial disclosures can be. Forms such as the 433-A or 433-B require:

- Verification of income

- Asset equity analysis

- Allowable expense calculations

- Bank and investment disclosures

Errors or omissions can lead to denial or enforcement escalation. A tax attorney evaluates financial standards, anticipates IRS scrutiny, and structures disclosures strategically — especially in hardship or business cases.

Negotiation Leverage and IRS Communication

When you call the IRS yourself, you are responsible for articulating eligibility, referencing Internal Revenue Code provisions, and responding to objections in real time. IRS representatives follow internal guidelines and may not volunteer relief options unless specifically requested.

A tax attorney communicates with the IRS on your behalf, cites relevant procedural authority, and escalates cases to Appeals when appropriate. Professional representation often changes the tone and structure of discussions.

Approval Rates and Strategic Positioning

While no outcome can be guaranteed, structured submissions supported by legal reasoning and documentation tend to reduce denial risk. DIY requests are sometimes denied due to incomplete evidence or technical errors rather than lack of eligibility.

Experienced representation focuses on presenting the strongest available legal basis from the beginning — whether penalty abatement, installment agreement negotiation, hardship status, or offer in compromise.

Time Investment and Stress Reduction

IRS matters require time: reviewing transcripts, gathering documentation, preparing forms, following up on hold times, and tracking deadlines. Many taxpayers underestimate the administrative burden.

Hiring a tax attorney shifts that workload to a professional team. This reduces stress and allows the taxpayer to focus on employment, business operations, or family responsibilities while the case is managed strategically.

Long-Term Compliance Planning

DIY resolutions often address the immediate problem but overlook long-term compliance strategy. A tax attorney can evaluate:

- Withholding adjustments

- Estimated tax planning

- Business payroll compliance

- Collection statute expiration considerations

Preventing recurrence is just as important as resolving the current issue.

The Bottom Line

For simple, low-risk cases, DIY resolution may be appropriate. But in 2026 , where enforcement moves faster and documentation standards remain strict , professional representation often provides procedural protection, structured negotiation, and reduced risk exposure. The complexity of the case, the amount owed, and the stage of enforcement should guide the decision.

Real-World Scenario (Hypothetical Case Example)

A 62-year-old taxpayer receiving Social Security owed $48,000. After submitting Form 433-F with documented medical expenses exceeding IRS standards, the account was placed in CNC. The IRS initially questioned transportation costs, but additional documentation resolved the issue.

Result: Garnishment avoided. Refunds offset. Debt aging toward CSED.

No guarantees , each case depends on documentation and financial profile.

Taxpayer Mistakes to Avoid in 2026

- Agreeing to unaffordable payment plans

- Failing to file missing returns

- Underreporting necessary expenses

- Ignoring Final Notice (LT11)

- Falling for “pennies on the dollar” scams

The tax relief industry has aggressive marketing. CNC eligibility is math-based — not marketing-based.

Why Experience Matters in IRS Cases

IRS collection is procedural and evidence-driven.

Experienced tax professionals understand:

- Revenue Officer discretion

- Allowable vs conditional expenses

- Internal hardship review thresholds

- Appeals procedures

- Statute expiration planning

In our experience representing taxpayers before Revenue Officers, presentation of financial data significantly impacts outcomes.

Take Action Before the IRS Escalates

Ignoring IRS notices increases risk.

If you are facing:

- Wage garnishment

- Bank levy

- Federal tax lien

- Final Notice of Intent to Levy

Early evaluation increases available options.

Confidential consultations are available.

Frequently Asked Questions

1. Does CNC erase my IRS debt?

No. The debt remains and interest accrues.

2. Can the IRS garnish my wages while in CNC?

Generally no, unless status is removed.

3. Will the IRS file a tax lien in CNC?

Possibly, especially if balance exceeds $10,000.

4. How often does the IRS review CNC cases?

Periodically, typically every 1–2 years.

5. Does CNC affect my credit?

CNC itself does not, but a filed tax lien may.

6. Can I apply for an Offer in Compromise while in CNC?

Yes, if you qualify.

7. What happens if my income increases?

The IRS may remove CNC and request payments.

Conclusion: Protect Your Financial Future Before the IRS Escalates

IRS collection matters rarely resolve themselves. Penalties grow, interest compounds daily, and enforcement actions can move faster than many taxpayers expect , especially in 2026, where automation and digital monitoring have shortened response timelines. What may begin as a balance-due notice can quickly escalate into wage garnishment, bank levies, or federal tax liens if not addressed strategically.

The key is not panic , it’s preparation.

Whether you are exploring penalty relief, installment agreements, hardship status, or another resolution option, timing and documentation matter. Small mistakes, missed deadlines, or incomplete disclosures can reduce your options and increase risk. On the other hand, early action often preserves appeal rights, limits enforcement exposure, and creates space for structured negotiation.

At Tax Law Advocates, our team of tax attorneys, CPAs, and enrolled agents has extensive experience representing individuals and businesses before the IRS. We understand how Revenue Officers evaluate financial disclosures, how Appeals Officers analyze risk, and how to position a case within IRS procedural guidelines. Every case is different , and we approach each one with detailed transcript review, compliance analysis, and strategic planning.

You do not have to navigate IRS enforcement alone.

If you’ve received a levy notice, are facing growing penalties, or simply want clarity about your options, now is the time to act. The earlier your case is evaluated, the more flexibility may be available.

Contact Tax Law Advocates today for a confidential, no-obligation consultation. Let us review your situation, explain your options clearly, and help you move forward with a plan designed to protect your financial stability , before the IRS takes the next step.

Important Legal Disclaimer (Updated 2026)

This content is for informational purposes only and does not constitute legal or tax advice. IRS outcomes depend on individual facts, documentation, and current enforcement policies. No result is guaranteed. Consult a licensed tax attorney, CPA, or enrolled agent regarding your situation.

About the Author: David Cho

As the Lead Tax Attorney at Tax Law Advocates, David Cho provides expert guidance on federal and state tax resolution matters. He earned both his J.D. and LL.M. in Taxation from the University of California, Irvine School of Law, building a strong foundation for his practice. David is passionate about delivering practical solutions that directly and positively impact his clients’ livelihoods, and he excels at working collaboratively with the IRS and state agencies to achieve favorable outcomes. His dedication is evident in his work, such as when he assisted a client who had fallen victim to a tax scam. By preparing and submitting a strategic Offer in Compromise, David helped her pursue resolution and take meaningful steps toward financial recovery. His deep knowledge of the IRS Debt Forgiveness Program makes him a vital resource for taxpayers facing significant challenges.