IRS Offer in Compromise is one of the most powerful tax debt relief programs available to struggling taxpayers, but it is also one of the most complex and frequently misunderstood. While the program allows qualified individuals and businesses to settle their tax debt for less than the full amount owed, the IRS applies strict financial scrutiny and compliance standards to every application.

As of 2026, the IRS has intensified documentation review, digital income verification, and cross-checking of bank deposits against reported earnings. In our experience representing taxpayers before Revenue Officers and the IRS Independent Office of Appeals, many IRS Offer in Compromise submissions are denied not because the taxpayer lacks hardship, but because of technical mistakes, incomplete disclosures, or preventable compliance issues.

At Tax Law Advocates, our licensed tax attorneys, CPAs, and enrolled agents have handled complex IRS collection cases nationwide. We routinely conduct detailed Reasonable Collection Potential (RCP) analyses, review asset equity calculations, and structure compliant IRS Offer in Compromise packages that align with current IRS Collection Financial Standards. We understand how Revenue Officers evaluate risk, how financial statements are audited, and how procedural errors can derail an otherwise qualified case.

An IRS Offer in Compromise is not simply a request for reduction, it is a formal legal settlement under Internal Revenue Code §7122 that requires full filing compliance, accurate financial documentation, realistic offer calculations, and ongoing tax compliance during review.

Before submitting an IRS Offer in Compromise, taxpayers should understand exactly how the IRS determines eligibility, what mistakes lead to rejection, and how experienced representation can significantly reduce avoidable risk.

What Is the IRS Offer in Compromise?

An Offer in Compromise (OIC) is a formal tax resolution program authorized under Internal Revenue Code §7122, allowing the Internal Revenue Service (IRS) to settle a taxpayer’s debt for less than the full amount owed. While many advertisements simplify the concept as “settling for pennies on the dollar,” the reality is far more technical. The IRS only approves an Offer in Compromise when strict legal and financial criteria are met.

An OIC is not a forgiveness program. It is a negotiated settlement based on a detailed financial analysis of your ability to pay. In our experience representing taxpayers before Revenue Officers and the IRS Independent Office of Appeals, successful Offers in Compromise require precise documentation, compliance with all filing requirements, and a carefully calculated settlement amount grounded in IRS methodology.

Below are the three legal grounds under which the IRS may accept an Offer in Compromise.

1. Doubt as to Collectibility (Most Common)

Doubt as to Collectibility is the most frequently used basis for an Offer in Compromise. This applies when the taxpayer’s assets and future income are insufficient to fully pay the tax liability within the statutory collection period (generally 10 years from assessment).

The IRS evaluates your Reasonable Collection Potential (RCP), which includes:

- Net equity in assets (real estate, vehicles, bank accounts, investments)

- Monthly disposable income after allowable expenses

- Future earning potential

- Dissipated assets (if applicable)

2. Doubt as to Liability

Doubt as to Liability applies when there is a legitimate dispute about whether the tax debt is actually owed. This situation may arise due to:

- Audit errors

- Misapplied payments

- Incorrect assessments

- Identity theft issues

- Documentation discrepancies

In these cases, the Offer in Compromise is not based on inability to pay, but on a disagreement regarding the accuracy of the assessed liability. Supporting evidence is critical, and this type of OIC requires detailed legal argument and documentation.

3. Effective Tax Administration

Effective Tax Administration (ETA) offers relief when the taxpayer technically has the ability to pay, but requiring full payment would create economic hardship or be unfair under exceptional circumstances.

Examples may include:

- Serious medical conditions

- Advanced age with limited income

- Situations where liquidation of assets would create extreme hardship

ETA cases are rare and require strong factual support. The IRS applies a high level of scrutiny to these applications.

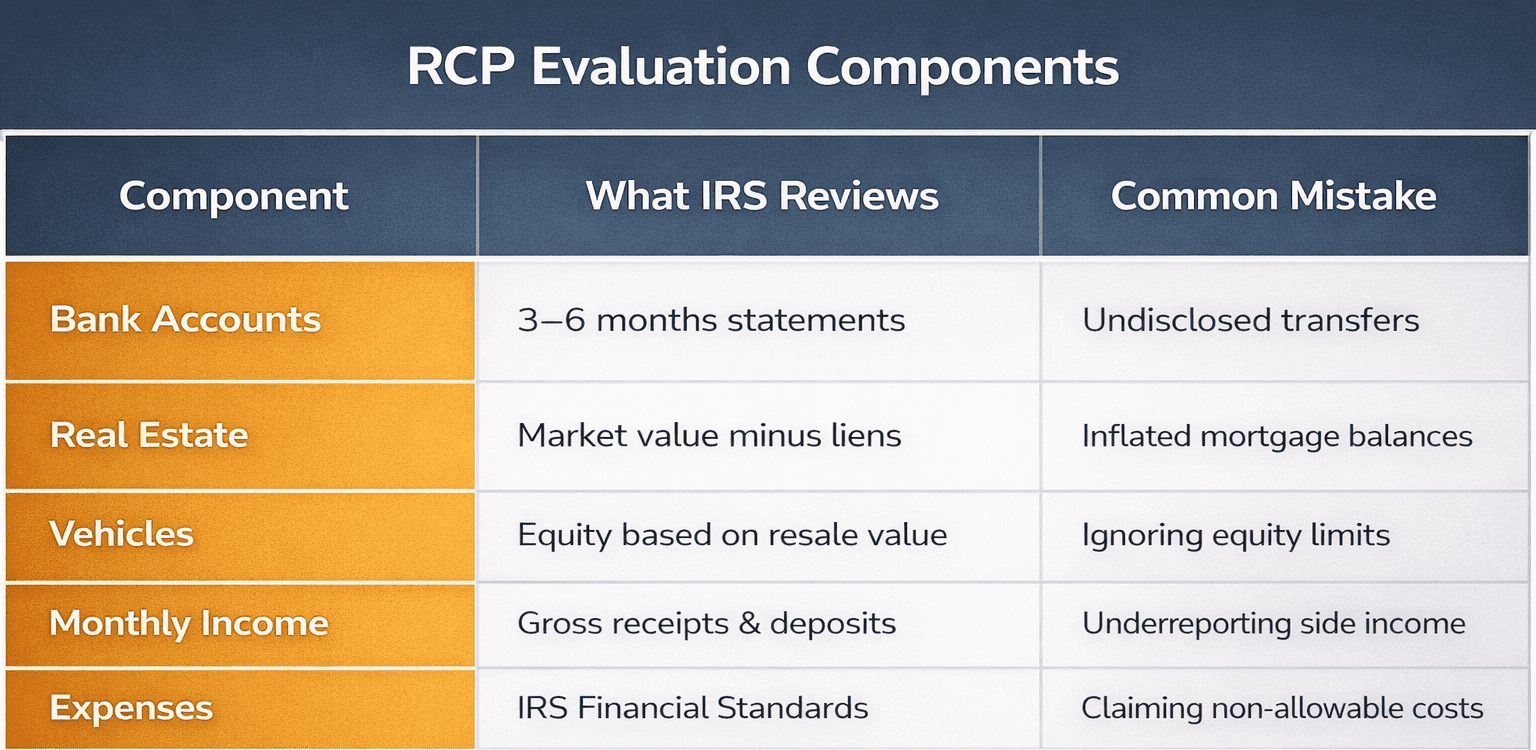

How the IRS Evaluates Reasonable Collection Potential (RCP)

Most Offers in Compromise are evaluated under the Reasonable Collection Potential (RCP) formula. This calculation determines the minimum amount the IRS believes it can collect through enforced collection methods such as levies or garnishments.

RCP generally includes:

- Quick-sale value of assets

- Monthly disposable income multiplied by a statutory factor (depending on payment method)

- Adjustments for allowable living expenses under IRS national and local standards

If your proposed offer equals or exceeds your calculated RCP, your chances of acceptance improve. If it falls significantly below, the IRS is likely to reject it.

Because the Offer in Compromise process involves legal standards, financial analysis, and strict compliance rules, professional evaluation is strongly recommended before submission.

Current IRS Enforcement Trends (2026 Update)

As of 2026, IRS enforcement activity continues to increase following multi-year funding expansions and modernization initiatives. The agency has invested heavily in technology, staffing, and data analytics, significantly improving its ability to identify noncompliance and collect unpaid tax debt.

One major trend in 2026 is enhanced digital financial verification. The IRS now cross-references bank deposit activity, third-party reporting (Forms 1099-K, 1099-NEC, W-2, brokerage statements), and prior-year return patterns more efficiently. Discrepancies between reported income and financial activity are flagged quickly, often triggering automated compliance notices or audit inquiries.

Another noticeable shift is increased scrutiny of high-balance collection cases, particularly those exceeding $250,000. Revenue Officers are actively assigned to larger accounts, and enforced collection tools, including wage garnishments, bank levies, and federal tax liens, are being deployed more consistently where taxpayers fail to engage.

The IRS has also strengthened compliance reviews in resolution programs such as Installment Agreements and Offers in Compromise. As of 2026, incomplete financial disclosures or missed current-year estimated tax payments can result in faster rejection or termination of pending relief arrangements.

Additionally, enforcement has expanded in areas involving:

- Cryptocurrency transaction reporting

- Gig economy and self-employment income

- Payroll tax enforcement for small businesses

- High-income non-filers

In our experience representing taxpayers nationwide, early intervention is more important than ever. The IRS is moving cases through the collection pipeline more efficiently, meaning ignored notices can escalate to levy action faster than in prior years.

The key takeaway for 2026: proactive compliance and accurate financial documentation are critical. Delays, incomplete filings, or unrealistic settlement proposals face increased scrutiny under current IRS enforcement practices.

Why the IRS Rejects Offer in Compromise Applications

An Offer in Compromise (OIC) can provide powerful tax debt relief, but the IRS rejects a significant percentage of applications each year. Contrary to popular belief, most rejections are not based solely on hardship eligibility. Instead, they stem from compliance gaps, inaccurate financial disclosures, or mathematical inconsistencies in the taxpayer’s Reasonable Collection Potential (RCP).

As of 2026, the IRS applies enhanced digital verification tools and strict documentation review standards. In our experience representing taxpayers before Revenue Officers, even minor errors can result in a returned or denied Offer in Compromise application.

Below are the primary reasons why the IRS rejects Offer in Compromise submissions.

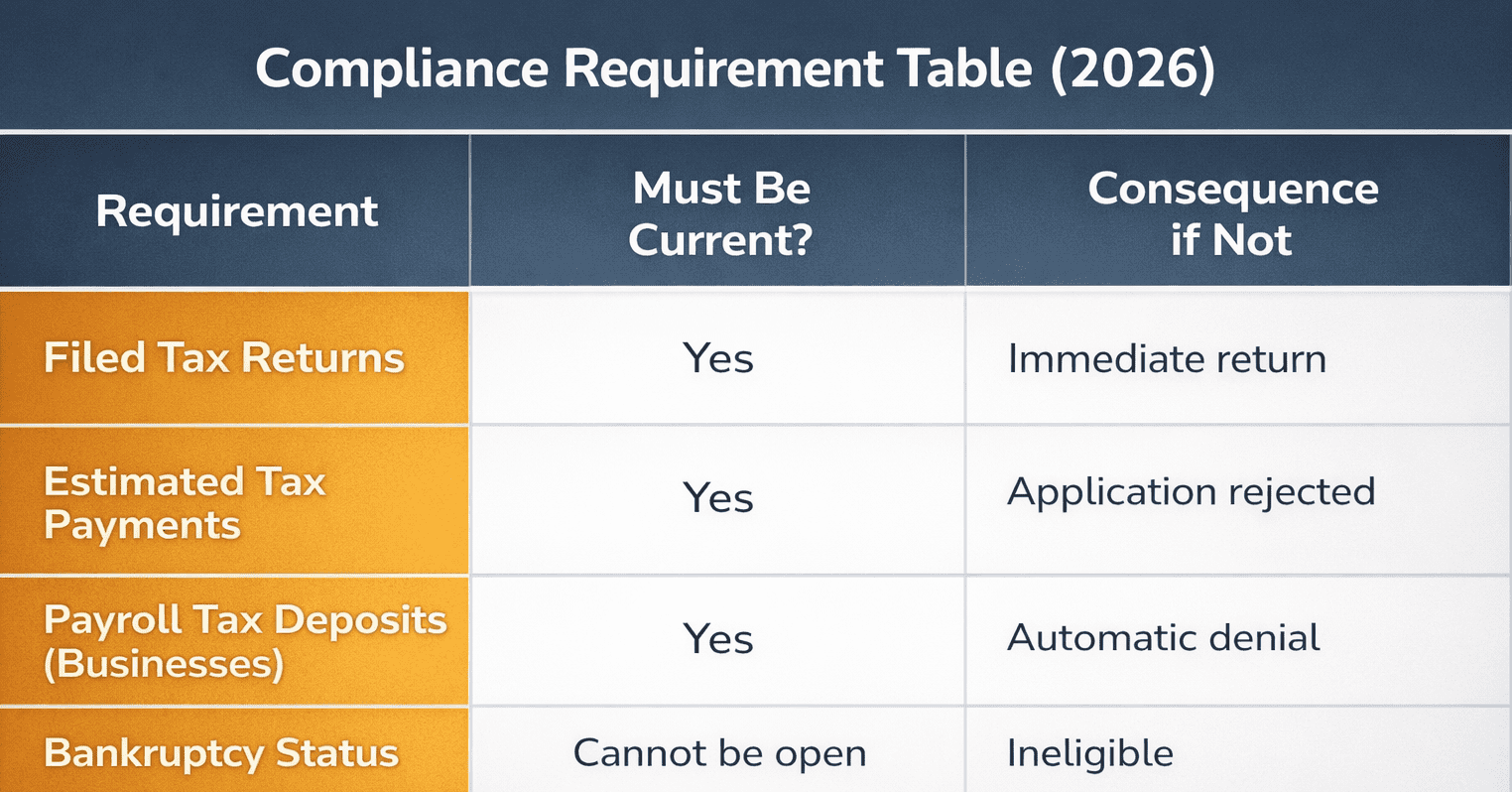

1. Failure to Meet Basic Eligibility Requirements

Before the IRS even evaluates financial hardship, it screens for compliance.

A taxpayer must:

- File all required tax returns

- Make current-year estimated payments (if self-employed)

- Maintain accurate withholding (if W-2 employee)

- Not be in an open bankruptcy proceeding

If any of these conditions are not met, the OIC will be returned without consideration.

2. Inaccurate Reasonable Collection Potential (RCP) Calculation

The most common technical reason the IRS rejects an Offer in Compromise is an incorrect RCP calculation.

RCP includes:

- Quick-sale value of assets

- Monthly disposable income

- Future earning potential

- Equity in real estate, vehicles, and investments

If the IRS determines your actual RCP exceeds your offer amount, it will deny the application.

3. Overstated Living Expenses

The IRS uses Collection Financial Standards to cap allowable expenses for:

- Housing

- Utilities

- Food

- Transportation

- Healthcare

If claimed expenses exceed these standards without justification, the IRS reduces allowable expenses, increasing your disposable income and raising your RCP.

This often results in rejection because the offer amount becomes too low compared to recalculated ability to pay.

4. Unrealistic or Bad-Faith Offer Amounts

Submitting a symbolic offer (for example, offering $1,000 on a calculated RCP of $25,000) signals noncompliance rather than hardship.

The IRS evaluates Offers in Compromise based on financial math, not emotional arguments.

Unrealistic offers are frequently denied without extended negotiation.

5. Missing Documentation or Deadlines

During review, the IRS may request:

- Updated bank statements

- Clarification of deposits

- Asset valuation documentation

- Verification of expenses

Failure to respond by deadline results in a returned offer, which cannot be appealed.

6.Ongoing Noncompliance During Review

Even after submission, taxpayers must remain compliant.

Common post-submission mistakes include:

- Missing quarterly payments

- Under-withholding wages

- Incurring new tax debt

If compliance breaks during review, the IRS may terminate consideration.

Financial Disclosure Mistakes in an IRS Offer in Compromise

One of the most common reasons the IRS rejects an IRS Offer in Compromise is inaccurate or incomplete financial disclosure. The OIC process requires taxpayers to submit detailed financial statements using Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses. These forms demand full transparency regarding income, assets, expenses, and liabilities. Even small inconsistencies can result in denial.

As of 2026, the IRS uses advanced digital cross-referencing tools to compare your disclosures against third-party reporting such as W-2s, 1099s, 1099-K payment processor records, brokerage statements, and prior-year returns. If your reported income does not align with bank deposits or lifestyle indicators, the IRS may recalculate your Reasonable Collection Potential (RCP) and reject your offer.

Common financial disclosure mistakes include:

- Failing to report all bank accounts or recent transfers

- Omitting cryptocurrency or investment holdings

- Undervaluing real estate or vehicles

- Inflating living expenses beyond IRS Collection Financial Standards

- Misclassifying personal expenses as business deductions

- Failing to disclose loans from family members

Another frequent issue is inconsistent documentation. For example, income listed on Form 433 may not match pay stubs or profit-and-loss statements. The IRS reviews at least three months of financial records and may request additional verification if discrepancies appear.

In our experience representing taxpayers nationwide, transparency and documentation accuracy are critical. Attempting to minimize reported assets or income often backfires, leading to recalculation and denial.

An IRS Offer in Compromise is evaluated on financial precision, not narrative hardship. Before submitting an application, taxpayers should carefully review every line item and ensure that supporting documentation aligns with IRS standards. Professional review can significantly reduce preventable errors and strengthen credibility during evaluation.

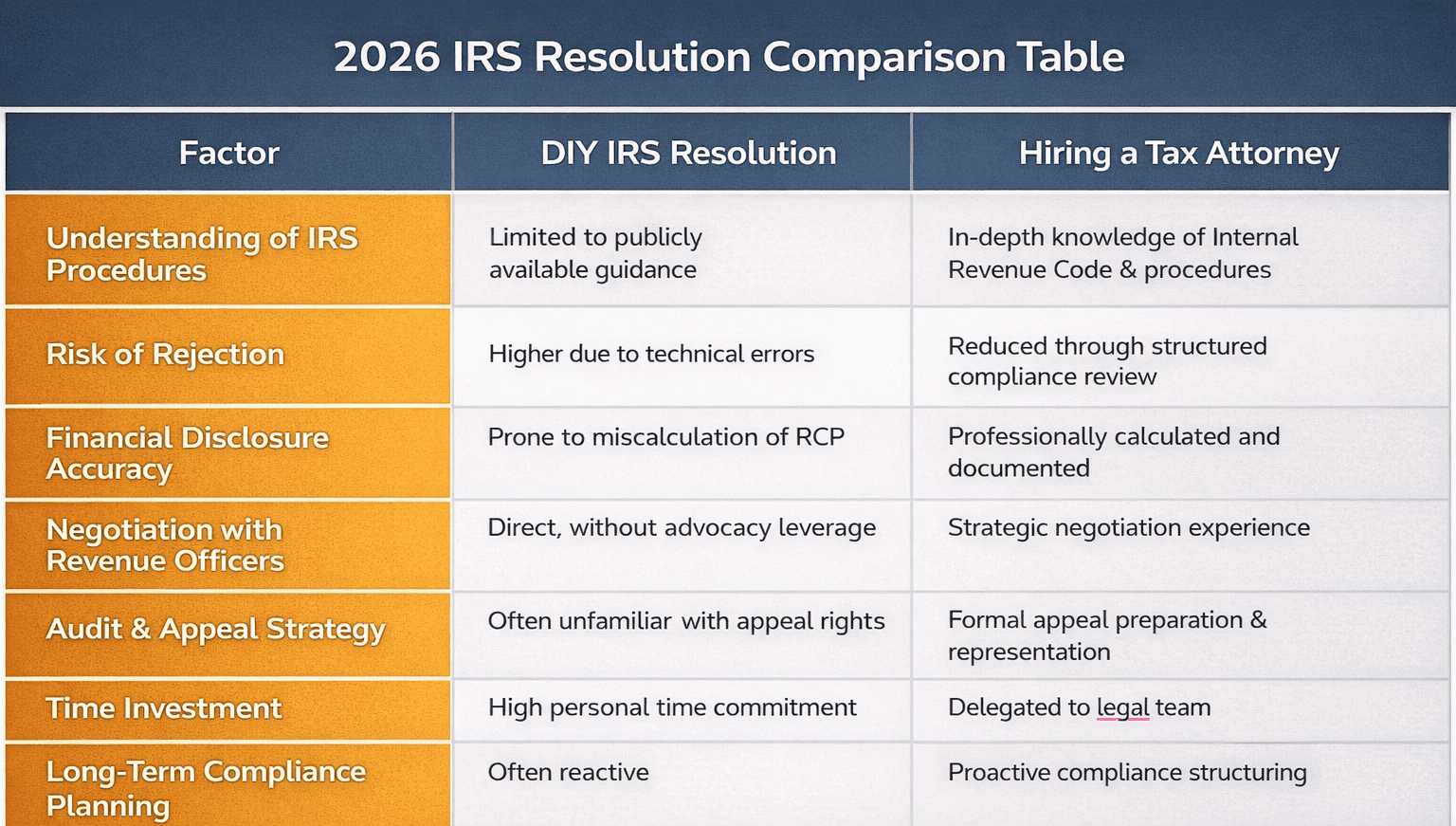

DIY IRS Resolution vs Hiring a Tax Attorney (2026 Comparison)

When facing serious tax debt, many taxpayers consider handling the IRS themselves to save money. While a DIY IRS resolution may work in limited, low-risk situations, complex cases, especially those involving an Offer in Compromise, high balances, payroll tax liabilities, or active enforcement, carry significantly greater risk.

As of 2026, IRS enforcement tools are more sophisticated. Revenue Officers use digital income verification, third-party reporting cross-checks, and strict procedural timelines. One missed deadline or inaccurate financial disclosure can result in levies, wage garnishments, or rejection of relief programs.

Below is a side-by-side comparison to help you evaluate the differences.

Risk Exposure Differences

A DIY approach may seem cost-effective initially, but errors can:

- Trigger recalculation of your Reasonable Collection Potential (RCP)

- Result in faster rejection of an Offer in Compromise

- Lead to termination of an Installment Agreement

- Escalate to levy or lien enforcement

Tax attorneys understand how the IRS interprets asset equity, allowable expenses, dissipated assets, and future income projections. They also recognize when alternative programs — such as Currently Not Collectible (CNC) status or a Partial Payment Installment Agreement, may be more appropriate than an Offer in Compromise.

When DIY May Be Reasonable

A self-representation approach may be reasonable when:

- The balance is relatively small

- You qualify for a streamlined installment agreement

- No Revenue Officer has been assigned

- There is no pending levy or enforcement action

However, once a case involves complex financial analysis or negotiation, professional guidance can significantly reduce preventable risk.

Key Consideration

Hiring a tax attorney does not guarantee approval, but experienced representation can:

- Ensure procedural compliance

- Strengthen financial documentation

- Reduce calculation errors

- Protect appeal rights

- Improve negotiation positioning

When IRS enforcement is active or tax debt is substantial, the cost of mistakes often exceeds the cost of professional representation.

Real Case Scenario: How an IRS Offer in Compromise Helped a Struggling Couple Resolve $148,000 in Tax Debt

In 2026, a married couple from California contacted our office after receiving a Final Notice of Intent to Levy. They owed approximately $148,000 in combined income tax, penalties, and interest accumulated over several years. The husband was self-employed in construction, and fluctuating income during the pandemic years led to missed estimated tax payments. The wife worked part-time and had modest W-2 wages.

They had previously attempted to submit an IRS Offer in Compromise on their own after seeing online advertisements promising “pennies on the dollar.” Unfortunately, their initial application was returned within four months. The IRS cited incomplete financial disclosures and recalculated their Reasonable Collection Potential (RCP) significantly higher than their proposed settlement.

When we reviewed their case, several issues were immediately apparent:

- They had overstated allowable housing expenses beyond IRS Collection Financial Standards.

- A business vehicle with equity had not been properly valued.

- Bank deposits were inconsistent with reported income.

- Quarterly estimated payments for the current year were not current during review.

As a result, their original IRS Offer in Compromise was deemed insufficient and non-compliant.

Our first step was ensuring full compliance. We brought all filings current, corrected their estimated tax payments, and conducted a detailed RCP recalculation using IRS methodology. After adjusting expenses to allowable standards and properly valuing assets using quick-sale value guidelines, their corrected RCP was calculated at $26,400, significantly lower than their total liability.

We then structured a revised IRS Offer in Compromise with comprehensive documentation, including:

- Three months of bank statements

- Profit-and-loss statements with deposit reconciliation

- Asset valuation support

- Written explanation of income volatility

During negotiations, the assigned Offer Specialist questioned certain deposits. We responded with supporting documentation showing transfers between accounts rather than unreported income. After approximately seven months of review, the IRS accepted the revised offer for $28,000 , payable over five months.

The couple avoided levy action, released collection pressure, and resolved $148,000 in tax debt for a fraction of the balance.

This case highlights a critical reality: an IRS Offer in Compromise is not simply about financial hardship. It requires precise documentation, compliance discipline, and accurate calculation under IRS standards. When structured correctly, however, it can provide legitimate and lasting tax relief.

IRS Offer in Compromise – FAQ (2026)

1. What is an IRS Offer in Compromise?

An IRS Offer in Compromise is a legal agreement that allows qualifying taxpayers to settle their tax debt for less than the full amount owed under Internal Revenue Code §7122.

2. Who qualifies for an IRS Offer in Compromise?

Taxpayers may qualify if they cannot pay their full tax debt through assets or future income, or if paying in full would create economic hardship. All required tax returns must be filed.

3.How does the IRS decide whether to accept an Offer in Compromise?

The IRS evaluates your Reasonable Collection Potential (RCP), which includes asset equity, monthly disposable income, and future earning ability.

4.Does the IRS really settle for “pennies on the dollar”?

Sometimes, but only if your financial documentation proves you cannot pay more. Approval depends on verified financial data, not advertising claims.

5. How long does an IRS Offer in Compromise take in 2026?

Most cases take 6 to 12 months, depending on complexity and IRS workload.

6. Does submitting an IRS Offer in Compromise stop collections?

Generally, active levy action pauses while the offer is under review, but interest and penalties continue accruing.

7. What causes an IRS Offer in Compromise to be rejected?

Common reasons include unfiled tax returns, inaccurate financial disclosures, unrealistic offer amounts, or failure to stay current on current-year taxes.

8. Can I appeal a rejected IRS Offer in Compromise?

Yes. You typically have 30 days to file an appeal using IRS Form 13711.

9. Do I need a tax attorney for an IRS Offer in Compromise?

Not legally required, but professional representation can help ensure compliance, accurate RCP calculation, and strategic negotiation.

10. What happens after my IRS Offer in Compromise is accepted?

You must comply with all tax filing and payment obligations for the next five years, or the IRS can reinstate the original debt.

Final Thoughts: Don’t Let IRS Offer in Compromise Mistakes Cost You Relief

An IRS Offer in Compromise can be one of the most powerful tools available for resolving serious tax debt , but only when it is prepared correctly, supported with accurate documentation, and structured according to IRS financial standards. As we’ve seen throughout this guide, most rejections are not caused by ineligibility alone. They are caused by preventable mistakes: unfiled returns, incorrect Reasonable Collection Potential (RCP) calculations, overstated expenses, missing documentation, or failure to remain compliant during review.

As of 2026, IRS enforcement and verification systems are more advanced than ever. Revenue Officers now cross-check bank deposits, asset transfers, third-party income reporting, and expense claims with increasing precision. Submitting an incomplete or unrealistic Offer in Compromise can delay relief for months , or even trigger renewed enforcement action.

In our experience representing taxpayers nationwide, successful IRS Offer in Compromise cases require strategy, compliance discipline, and professional presentation. It is not just about proving hardship. It is about aligning your financial reality with IRS methodology and negotiating from a position of credibility.

If you are considering an IRS Offer in Compromise, do not risk rejection by guessing at the numbers or relying on generic online advice.

Call Tax Law Advocates at 855-612-7777

Visit www.taxlawadvocates.com

Schedule your Free OIC Risk-Check Review today. Our licensed tax attorneys, CPAs, and enrolled agents will evaluate your eligibility, calculate your realistic settlement potential, and help you avoid costly mistakes before you file.

The IRS process is technical. Your resolution strategy should be, too.

Tax Law Advocates , Protecting Taxpayers Nationwide with Experience, Precision, and Integrity.

Important Legal Disclaimer (Updated 2026)

This content is for informational purposes only and does not constitute legal or tax advice. Every IRS case depends on specific facts, compliance history, and documentation. No outcome can be guaranteed. Consult a licensed tax attorney, CPA, or enrolled agent regarding your situation.